“You have a PhD in your field. You’ve read the financial statements. You’ve back-tested your strategy. Yet you still buy high, sell low, and hold losers too long. The problem isn’t your intelligence. It’s your biology.”

Behavioral finance biases are systematic psychological errors that cause investors and traders to make irrational financial decisions, even when they possess accurate data, tested strategies, and domain expertise. Behavioral finance is the study of how these biases influence investment decision-making, explaining why markets consistently deviate from the rational expectations assumed by traditional economic theory. This guide defines the field, classifies all major bias types, quantifies their impact on trading performance, and presents a structured framework for reducing their operational damage.

What Is Behavioral Finance?

Behavioral finance is the study of how psychological biases and cognitive errors influence investment decision-making, explaining why markets consistently deviate from the rational expectations of traditional economic theory. The field emerged from the work of psychologists Daniel Kahneman and Amos Tversky, whose 1979 Prospect Theory demonstrated that investors systematically violate rational utility models (Kahneman & Tversky — “Prospect Theory: An Analysis of Decision under Risk,” Econometrica, 1979).

Behavioral finance addresses four questions that traditional economic models cannot answer:

- Why do investors hold losing positions past rational exit points?

- Why do investors sell winning positions before their full potential is realized?

- Why do speculative bubbles and market crashes form repeatedly across generations?

- Why does past performance consistently fail to predict future results?

Behavioral Finance vs. Traditional Finance: The Rational Actor Myth

Traditional finance assumes investors are rational wealth-maximizers who process all available information objectively. Behavioral finance demonstrates that investors rely on heuristics, emotional shortcuts, and cognitive patterns that produce systematic, predictable errors. Modern Portfolio Theory, developed by Harry Markowitz in 1952, and Eugene Fama’s Efficient Market Hypothesis (1970) both rest on the rational actor assumption, that asset prices reflect all available information because market participants process it without bias (Markowitz — “Portfolio Selection,” Journal of Finance, 1952; Fama — “Efficient Capital Markets,” Journal of Finance, 1970).

Richard Thaler’s Nobel Prize in Economics (2017) recognized behavioral finance’s demonstration that systematic market inefficiencies exist precisely because this assumption fails (The Nobel Prize — Richard H. Thaler, 2017).

| Dimension | Traditional Finance | Behavioral Finance |

| Core Assumption | Investors are rational wealth-maximizers | Investors are emotional, biased, and irrational |

| Decision-Making Basis | All available information | Heuristics and mental shortcuts |

| Market Outcome | Efficient markets, fair pricing | Inefficient markets, mispricing, bubbles |

| Key Proponents | Fama, Sharpe, Markowitz | Kahneman, Tversky, Thaler, Shiller |

| Primary Goal | Maximize risk-adjusted returns | Identify and overcome psychological errors |

The Two Pillars of Bias: Cognitive Errors vs. Emotional Biases

Behavioral finance divides all investment biases into two categories: cognitive errors, which result from faulty reasoning or information processing, and emotional biases, which arise from impulse, intuition, or feeling. The CFA Institute’s behavioral finance curriculum formalizes this two-pillar taxonomy as the foundation for bias identification and intervention (CFA Institute — Behavioral Finance Curriculum).

Cognitive Errors: The Faulty Wiring

Cognitive errors result from basic statistical, information processing, or memory failures, not emotional states. The CFA Institute identifies 6 cognitive error subtypes across 2 categories:

- Belief Perseverance Biases: errors in updating beliefs when new evidence arrives, including confirmation bias, representativeness, and conservatism bias

- Information Processing Biases: errors in how data is analyzed and weighted, including anchoring, mental accounting, framing, and the availability heuristic

Cognitive errors are theoretically correctable through education and structured System 2 reasoning because they originate in identifiable reasoning failures rather than emotional states (Corporate Finance Institute — Behavioral Finance).

Emotional Biases: The Heart Over the Head

Emotional biases stem from feelings and intuition rather than conscious reasoning, making them harder to correct than cognitive errors. The CFA Institute identifies 5 primary emotional biases in investment behavior:

- Loss aversion

- Overconfidence

- Herd behavior

- Endowment effect

- Regret aversion

Emotional biases originate in System 1 automatic processing: Kahneman (2011) identifies emotional biases as the hardest category to correct because structural triggers, not information alone, are required to activate the System 2 reasoning that overrides them (Kahneman — Thinking, Fast and Slow, 2011).

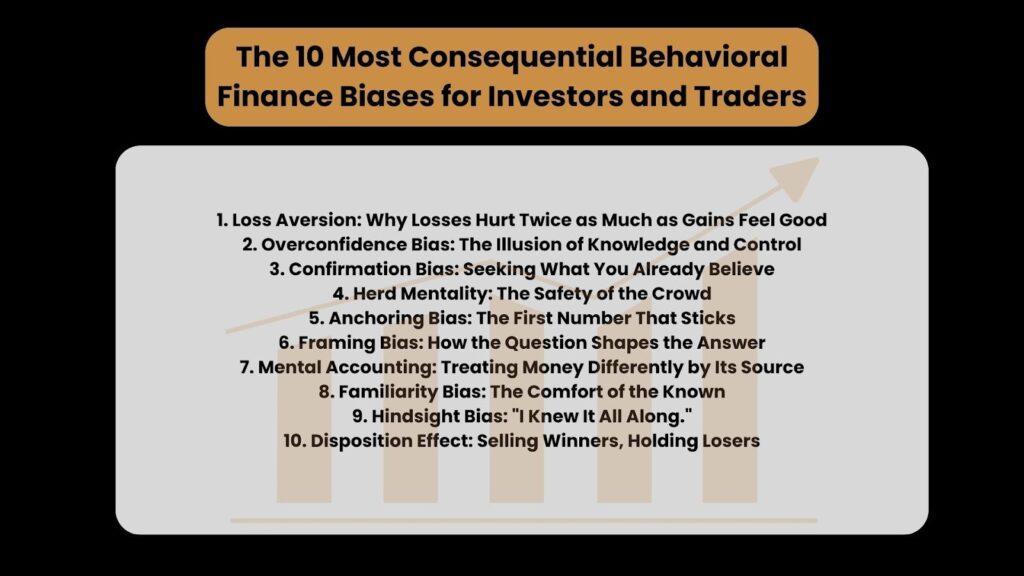

The 10 Most Consequential Behavioral Finance Biases for Investors and Traders

The 10 most consequential behavioral finance biases for investors and traders are loss aversion, overconfidence bias, confirmation bias, herd mentality, anchoring bias, framing bias, mental accounting, familiarity bias, hindsight bias, and the disposition effect.

| Bias | Type | Core Impact | De-biasing Action |

| Loss Aversion | Emotional | Holds losers, exits winners too early | Pre-set stop-losses at entry |

| Overconfidence | Cognitive | 45% more trading, 2.65% return drag | Trading journal with prediction tracking |

| Confirmation Bias | Cognitive | Filters out disconfirming data | Pre-trade devil’s advocate checklist |

| Herd Mentality | Emotional | Buys tops, sells bottoms | Quantitative model, independent thesis |

| Anchoring Bias | Cognitive | Fixates on purchase price over fundamentals | Evaluate on current data only |

| Framing Bias | Cognitive | Same data, different frame, different decision | Restate every decision in both gain and loss terms |

| Mental Accounting | Cognitive | Higher risk-taking with “house money.” | Treat all capital as identical in value |

| Familiarity Bias | Emotional | 70–80% domestic equity concentration | Systematic allocation across sectors and geographies |

| Hindsight Bias | Cognitive | Inflates confidence in predictive ability | Dated trading journal reviewed pre-outcome |

| Disposition Effect | Emotional | Sells winners 50% more often than losers | Pre-define exit rules at trade entry |

1. Loss Aversion: Why Losses Hurt Twice as Much as Gains Feel Good

Loss aversion is a cognitive bias in which the pain of a loss registers approximately twice as intensely as the pleasure of an equivalent gain (Kahneman & Tversky — Prospect Theory, Econometrica, 1979), Econometrica, 1979). Loss-averse investors hold losing positions past rational exit points while exiting winning positions early, producing an estimated 1–2% annual performance drag.

Trader application: A trader holds a position down 20% because selling makes the loss permanent, while identical capital sits idle and misses recovery opportunities elsewhere.

Neuroscience: Tom et al. (2007) used fMRI to confirm that potential losses activate the striatum and ventromedial prefrontal cortex more intensely than equivalent gains, the neural asymmetry that produces loss aversion’s 2:1 pain ratio (Tom et al. — “The Neural Basis of Loss Aversion in Decision-Making Under Risk,” Science, 2007).

De-biasing: Pre-commit to stop losses at trade entry and treat each position as an independent decision isolated from the entry price.

2. Overconfidence Bias: The Illusion of Knowledge and Control

Overconfidence bias describes the tendency of investors to overestimate their knowledge, predictive accuracy, and control over market outcomes. Barber and Odean (2000) found that overconfident investors trade 45% more frequently than investors operating within rational confidence bounds, reducing net annual returns by 2.65% through transaction costs and poor timing (Barber & Odean — “Trading Is Hazardous to Your Wealth,” Journal of Finance, 2000).

Trader application: An overconfident trader takes an oversized position on a high-conviction thesis while dismissing contradictory technical signals.

Neuroscience: Winning streaks activate dopaminergic reward circuits, reinforcing risk-seeking behavior in subsequent decisions, a pattern Kahneman (2011) identifies as a System 1 reward feedback loop that amplifies overconfidence independently of actual predictive accuracy.

De-biasing: Maintain a dated trading journal that tracks predictions separately from outcomes. Review forecast accuracy monthly.

3. Confirmation Bias: Seeking What You Already Believe

Confirmation bias describes the tendency to search for, interpret, and recall information that confirms pre-existing beliefs while ignoring contradictory evidence. Wason (1960) first demonstrated this in his selection task experiments, establishing it as a systematic reasoning failure rather than random error (Wason — “On the Failure to Eliminate Hypotheses in a Conceptual Task,” Quarterly Journal of Experimental Psychology, 1960).

Investors affected by confirmation bias spend 67% more time reading analysis that supports their existing positions than analysis that challenges them.

Confirmation bias manifests in trading when a trader entering a long position reads only bullish commentary and dismisses deteriorating volume data that directly contradicts the thesis.

Cognitive dissonance, identified by Festinger (1957), triggers discomfort when contradictory information is encountered. The brain reduces this discomfort by discounting challenging data rather than updating the belief, a neural efficiency shortcut that systematically distorts information processing.

A written devil’s advocate argument before every trade entry provides a structured search for the strongest case against the position, directly interrupting the confirmation bias cycle.

4. Herd Mentality: The Safety of the Crowd

Herd mentality describes the tendency to follow the actions of a larger group, abandoning independent analysis in favor of social consensus. Shiller (2000) identified herd behavior as the primary driver of speculative bubbles, documenting how collective overconfidence drove technology stock valuations to 5–10× sustainable levels before the NASDAQ fell 78% from its March 2000 peak (Shiller — Irrational Exuberance, Princeton University Press, 2000).

Trader application: A trader buys a meme stock at peak price because social media consensus creates the perception of a guaranteed directional move.

Neuroscience: Eisenberger et al. (2003) established that social ostracism activates the dorsal anterior cingulate cortex, the same region activated by physical pain, making crowd behavior neurologically reinforcing because following the herd avoids this pain signal (Eisenberger et al. — “Does Rejection Hurt? An fMRI Study of Social Exclusion,” Science, 2003).

De-biasing: Define position theses using quantitative criteria before checking social sentiment. Set maximum position size limits independent of crowd behavior.

5. Anchoring Bias: The First Number That Sticks

Anchoring bias describes the tendency to fixate on a specific reference point, typically the first price encountered, and fail to adjust valuations sufficiently as new information emerges (Tversky & Kahneman — “Judgment Under Uncertainty: Heuristics and Biases,” Science, 1974).

Investors anchored to a stock’s 52-week high wait an average of 2–3 years for price recovery, forfeiting reallocation opportunities elsewhere.

Trader application: A trader refuses to exit a position that has dropped 35% below entry because the purchase price serves as the psychological floor for acceptable outcomes.

Neuroscience: The prefrontal cortex encodes initial reference points as cognitive anchors. Kahneman (2011) identifies anchor adjustment as a System 2 task that automatic System 1 processing consistently bypasses, keeping investors locked to irrelevant historical prices.

De-biasing: Evaluate every open position using current fundamentals and forward projections only. Purchase price is not a valid data point for exit decisions.

6. Framing Bias: How the Question Shapes the Answer

Framing bias describes how the same information, presented as a gain versus a loss, produces different decisions, even when the underlying data is identical (Tversky & Kahneman, “The Framing of Decisions and the Psychology of Choice,” Science, 1981).

In Tversky and Kahneman’s (1981) experiments, a 90% survival rate and a 10% mortality rate, mathematically identical probabilities, produced statistically different choices across subjects.

Trader application: A trader views a strategy with a 90% win rate as low-risk while rejecting an identical strategy described as carrying a 10% loss rate, ignoring that the risk-reward ratio is unchanged.

Neuroscience: De Martino et al. (2006) confirmed using fMRI that loss-framed decisions activate the amygdala’s threat response while gain-framed decisions engage reward circuitry, producing neurologically distinct decision states from identical information (De Martino et al. — “Frames, Biases, and Rational Decision-Making in the Human Brain,” Science, 2006).

De-biasing: Restate every trading decision in both gain and loss terms before committing. A decision that changes based on framing is controlled by presentation, not evidence.

7. Mental Accounting: Treating Money Differently by Its Source

Mental accounting is the tendency to treat money differently based on its source, intended use, or psychological account (Thaler — “Mental Accounting Matters,” Journal of Behavioral Decision Making, 1999).

Richard Thaler introduced the concept in 1985. Investors exposed to mental accounting increase risk exposure by 15–20% after a winning streak. Winning streak gains occupy a separate psychological account — “house money” — with lower loss-aversion thresholds than original capital.

Investors increase risk exposure by 15–20% after a winning streak, treating gains as psychologically separate “house money” with lower loss-aversion thresholds than original capital.

Trader application: After a profitable month, a trader risks 30% of the account on a single speculative position, rationalizing it as playing with the market’s money.

Neuroscience: Mental accounts function as psychological cost centers. Thaler (1999) demonstrates that each account carries its own loss-aversion threshold independent of actual dollar value, producing differential risk tolerance across capital pools of identical size.

De-biasing: Treat all capital as identical in value regardless of origin. Apply the same position sizing rules to gains as to original capital.

8. Familiarity Bias: The Comfort of the Known

Familiarity bias describes the tendency to prefer assets that investors recognize, such as domestic stocks, employer equity, or industries they work in, over unfamiliar alternatives that deliver superior risk-adjusted returns in documented diversification studies. French and Poterba (1991) documented that investors hold 70–80% domestic equities despite international diversification reducing portfolio volatility (French & Poterba — “Investor Diversification and International Equity Markets,” American Economic Review, 1991).

Trader application: A trader allocates 85% of capital to technology stocks because professional familiarity with the sector creates an illusion of informational edge.

Neuroscience: Familiarity reduces perceived risk through processing fluency. Zajonc’s (1968) mere exposure research established that cognitive ease of processing is encoded as a positive safety signal independent of actual risk metrics, meaning the brain rates familiar assets as safer simply because they are easier to process.

De-biasing: Apply systematic allocation models that enforce geographic and sector diversification independent of personal familiarity or comfort level.

9. Hindsight Bias: “I Knew It All Along.”

Hindsight bias describes the tendency to perceive past events as having been predictable, distorting post-event memory to align with known outcomes and inflating confidence in future predictive ability. Fischhoff (1975) established that outcome knowledge systematically distorts retrospective probability estimates, a retrospective distortion he termed the “knew-it-all-along effect,” where certainty of outcome knowledge directly correlates with the magnitude of probability inflation (Fischhoff — “Hindsight ≠ Foresight,” Journal of Experimental Psychology, 1975).

Trader application: After a market correction, a trader recalls general bearish sentiment as a specific, actionable prediction and increases leverage by 2–3× before the next anticipated move, a position size unjustified by any pre-event documented thesis.

Neuroscience: Memory reconstruction is an active neural process. Fischhoff (1975) identifies retroactive distortion as the mechanism converting post-event clarity into false predictive confidence, where the brain systematically replaces pre-event uncertainty with the narrative coherence of known outcomes.

De-biasing: Maintain a dated trading journal with explicit predictions recorded before market events. Review entries before checking outcomes to preserve pre-event reasoning.

10. Disposition Effect: Selling Winners, Holding Losers

The disposition effect describes the systematic tendency to sell assets that have increased in value while holding assets that have declined, identified by Shefrin and Statman in 1985 as the direct opposite of the “cut losses short, let profits run” principle (Shefrin & Statman — “The Disposition to Sell Winners Too Early and Ride Losers Too Long,” Journal of Finance, 1985).

Shefrin and Statman found that investors are 50% more likely to sell a winning position than a losing position on any given trading day.

Trader application: A trader exits a position up 8% to lock in gains while simultaneously holding three losing positions averaging −22%, violating the core rule of capital preservation.

Neuroscience: The disposition effect combines loss aversion, the reluctance to realize losses, with the hedonic pleasure of locking in gains. These two distinct emotional drivers reinforce a single destructive trading pattern, operating through separate neural mechanisms that converge on the same behavior.

De-biasing: Pre-define exit rules for both winning and losing positions at trade entry. Use trailing stops for winners and fixed stop-losses for losers. Remove real-time emotional discretion from exit decisions entirely.

How Biases Create Market Anomalies: Bubbles, Crashes, and Momentum

When behavioral finance biases aggregate across millions of investors simultaneously, they produce predictable market anomalies, including speculative bubbles, panic-driven crashes, and momentum effects that the Efficient Market Hypothesis cannot explain. Thaler’s (2016) retrospective confirmed that these anomalies are systematic, repeatable consequences of identifiable psychological patterns, not random noise (Thaler — “Behavioral Economics: Past, Present, Future,” American Economic Review, 2016).

Four major market anomalies map directly to specific bias combinations:

- Bubbles: Herd Mentality + Overconfidence + Confirmation Bias drive collective overvaluation. Shiller’s cyclically adjusted P/E ratio reached 44 in January 2000, more than double its historical average of 17, before the dot-com collapse.

- Crashes: Loss Aversion + Herd Behavior + Panic selling accelerate price collapse beyond fundamental value. On Black Monday (October 19, 1987), the DJIA fell 22.6% in a single session, consistent with loss aversion-driven panic amplification rather than rational revaluation.

- Momentum Effect: Herding + Anchoring + Disposition Effect sustain price trends past rational inflection points. Jegadeesh and Titman (1993) documented that momentum strategies generated average returns of 1% per month over 25 years (Journal of Finance, 1993).

- Value vs. Growth Anomalies: Familiarity Bias + Mental Accounting systematically underprice unfamiliar assets. Fama and French (1992) documented that value stocks outperformed growth stocks by an average of 4.9% annually from 1963 to 1990 (Journal of Finance, 1992).

Biases in Modern Markets: Crypto, Meme Stocks, and Algorithmic Trading

Behavioral finance biases are not limited to traditional equity markets. Cryptocurrency markets, meme stocks, and algorithmic trading environments amplify these biases because they remove the structural safeguards present in regulated exchanges.

Crypto Markets: The Perfect Storm of Biases

Cryptocurrency markets concentrate three of the most destructive behavioral finance biases, FOMO-driven herd mentality, overconfidence in volatility trading, and anchoring to all-time highs, into a single 24/7 environment with no circuit breakers, no trading halts, and no cooling-off mechanisms. Bitcoin declined 83% from its December 2017 peak of approximately $19,800 to $3,200 by December 2018, a trajectory consistent with the herd-driven speculative overvaluation Shiller (2000) identified as the structural cause of bubble formation.

Three bias patterns dominate crypto market behavior:

- Herd Mentality via FOMO: social media amplification drives coordinated buying into price peaks

- Overconfidence in volatility: high short-term returns reinforce the dopamine feedback loop, producing the excess trading frequency that Barber and Odean (2000) documented in overconfident investor populations

- Anchoring to all-time highs: investors hold depreciated positions for years, anchored to peak prices as recovery targets rather than current fundamentals

Meme Stocks: Herd Behavior in the Social Media Age

The GameStop and AMC trading events of January 2021 represent herd mentality amplified by social media coordination, where retail investor herding on Reddit’s WallStreetBets drove prices to levels disconnected from fundamental valuation. GameStop reached a peak price of $483 on January 28, 2021, a 2,700% increase from its price three weeks earlier, before declining 90% within weeks, following the bubble-and-crash pattern Shiller (2000) identified as the structural outcome of collective herd behavior. The GameStop episode demonstrated that social media reduces the coordination cost of herding to near zero, compressing bubble formation timescales from months to days.

Algorithmic Trading: When Human Biases Meet Machine Execution

Algorithmic trading systems do not carry emotional biases, but the humans who design, optimize, and deploy them introduce cognitive errors into automated execution. Kahneman (2011) establishes that cognitive errors persist in expert decision-making even when practitioners are aware of them, a finding directly applicable to quantitative developers who overfit models to historical data while maintaining high forward-performance confidence. Three cognitive errors enter through algorithm design:

- Backtesting bias: the systematic overestimation of a strategy’s future performance based on its historical fit, consistent with the overconfidence patterns Barber and Odean (2000) documented in active traders

- Over-optimization: excessive parameter tuning eliminates model robustness by fitting to historical noise rather than signal, producing systems fragile to regime change

- Black-box overconfidence: misplaced certainty in algorithmic outputs whose failure conditions the operator does not understand, a direct extension of the overconfidence bias Kahneman (2011) identifies as persistent in expert populations

De-biasing: A Systematic Framework for Better Decisions

De-biasing is the process of reducing the impact of cognitive and emotional biases on investment decisions through structured systems, pre-commitment rules, and process-oriented review, not willpower or awareness alone.

Awareness Is Not Enough

Knowing about a bias does not prevent it. Kahneman (2011) documents that even behavioral economists who teach bias recognition remain fully susceptible to the biases they study. Bias originates in System 1 automatic processing; structural triggers, not awareness, are required to activate the System 2 reasoning that overrides it.

The M1 De-biasing Framework: Three Layers of Protection

The M1 de-biasing framework applies three sequential layers of protection: pre-commitment rules defined before trade entry, systematic pre-trade checklists, and post-trade process reviews focused on decision quality rather than P&L outcome. Pre-commitment devices represent the most reliable behavioral intervention identified in the literature, the operational foundation of rules-based investing (Thaler & Sunstein — Nudge, Yale University Press, 2008).

- Layer 1, Pre-Commitment: Define stop-loss levels, profit targets, and maximum position sizes before entering any trade. Rules established before emotional exposure are more durable than discretionary decisions made during live market conditions.

- Layer 2, Pre-Trade Checklist: Complete a structured checklist that forces evaluation of contradictory evidence, position sizing rationale, and bias exposure before execution, bypassing emotional shortcuts with a systematic process.

- Layer 3, Process Review: Conduct post-trade analysis focused on checklist adherence and decision process quality. Evaluating process rather than P&L outcome breaks the reinforcement loop that reward-based review creates.

Tools for De-biasing

Five systematic tools reduce the operational impact of behavioral finance biases on investment decisions. Kahneman (2011) identifies structured external aids as the primary mechanism for activating System 2 reasoning in environments where System 1 dominates. Thaler and Sunstein (2008) classify pre-commitment tools and choice architecture as the most durable behavioral change mechanisms available:

- Trading journals: dated prediction entries reviewed before outcome checks preserve pre-event reasoning and interrupt hindsight bias reconstruction

- Decision trees: force structured enumeration of outcomes and probability estimates before commitment, activating System 2 evaluation

- Second-order thinking prompts: the question “And then what?” surfaces downstream consequences that System 1 automatic processing ignores

- Devil’s advocate protocols: mandatory counter-thesis construction before every entry directly counters the selective reading pattern Wason (1960) documented, where investors spend 67% more time on confirming analysis than disconfirming analysis

- Algorithmic execution rules: pre-programmed entry, exit, and sizing parameters remove real-time emotional discretion from execution entirely

The M1 Approach: From Bias Awareness to Systematic Execution

Understanding behavioral finance biases is the first step. Building a personalized system that protects against them in real trading conditions is the second, and operationally harder step. Bias profiles differ across individuals: a trader with high loss aversion requires different interventions than one whose primary error is overconfidence. The M1 Process provides a personalized framework for identifying an individual’s bias profile and implementing systematic de-biasing protocols calibrated to their specific trading style and risk psychology. The process translates behavioral finance research into behavioral portfolio management protocols, not general awareness programs.

Conclusion

Behavioral finance biases are not character flaws. They are biological facts embedded in neural architecture that evolved for survival in environments where fast, pattern-based decisions were adaptive. Financial markets punish those same automatic responses. The goal is not to eliminate behavioral finance biases, that is, neurologically impossible, but to build decision systems that interrupt their automatic execution at the critical moments of trade entry, management, and exit. Systematic protection, applied consistently across the trader’s decision lifecycle, is the operational difference between knowing about bias and being protected from it.

Frequently Asked Questions

What is behavioral finance in simple terms? Behavioral finance is the study of how psychological biases cause investors to make irrational financial decisions despite having access to accurate information. The field, founded by Daniel Kahneman and Amos Tversky in 1979, explains market anomalies that rational actor models cannot account for.

What are the two main types of behavioral finance biases? The two main types of behavioral finance biases are cognitive errors, which result from faulty information processing, including anchoring, framing, and confirmation bias, and emotional biases, which arise from impulse and intuition, including loss aversion, overconfidence, and herd behavior. The CFA Institute formalizes this two-category taxonomy as the foundation for bias identification and intervention.Can behavioral finance biases be eliminated? Behavioral finance biases cannot be eliminated because they originate in automatic neural processes that operate below conscious awareness. Their impact on investment decisions is reduced through pre-commitment rules, structured checklists, and process-oriented post-trade review, systematic interventions that activate deliberate reasoning before emotional responses are executed.